2018 San Diego Real Estate Market Analysis

2018 San Diego Real Estate Market Analysis

San Diego County Residential Real Estate Market Analysis: 1st Quarter 2018

By Mark A. Melikian California Certified Residential Appraiser appraisals@san.rr.com P.O. Box 3051 Del Mar, California 92014 858-945-8996 ©2018

The following is a market data summary of detached and attached properties as reported by the San Diego County MLS system. The data includes all zip codes in San Diego County. All projections discussed in this analysis will be updated throughout the year in subsequent quarterly reports.

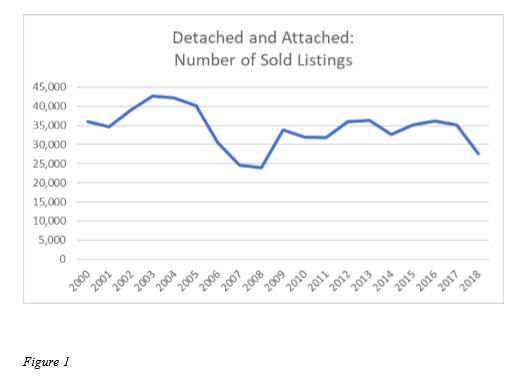

Market Overview: The data provided analyzes residential real estate sales beginning in the year 2000, which is used as the base year. The number of sold listings in San Diego County peaked in 2003 at 42,746 units and decreased through 2008 to 23,972 units. In 2018, the total number of units sold, based on first quarter results, is projected to be 27,596, down from 35,200 sales in 2017 (see Figure 1).

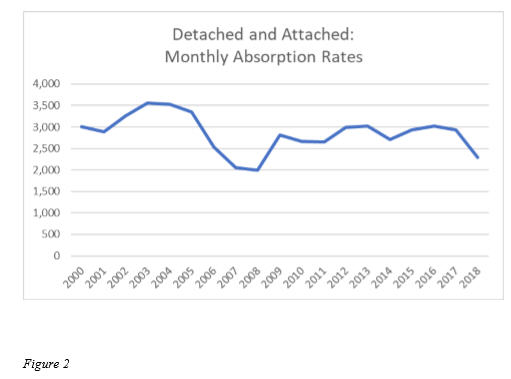

Market Overview: The monthly absorption rate (number of units sold in a month) will mirror the trend we see in the number of sold listings. The peak monthly absorption rate occurred in 2003 with 3,562 units selling per month. In 2008, the monthly absorption rate decreased to a low of 1,998 units. The 2018 projected monthly absorption rate, based on first quarter results, is 2,300 units, down from 2,933 units in 2017 (see Figure 2).

2018 San Diego Real Estate Market Analysis

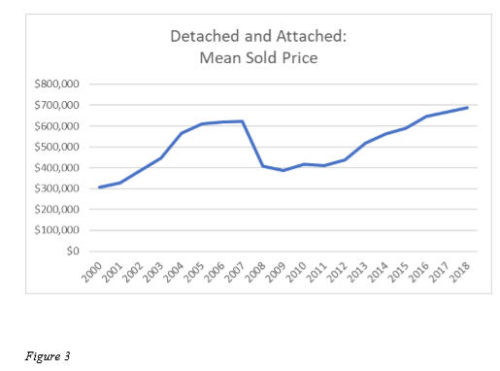

Market Overview: The mean sold price for a housing unit in San Diego County is projected to reach a new high this year, based on first quarter results. The current 2018 projection is for a mean sale price of $689,017. This would surpass the previous peak of $666,903 set in 2017. The currently projected mean sold price reflects a 3.3 percent increase over last year’s mean sold price (see Figure 3).

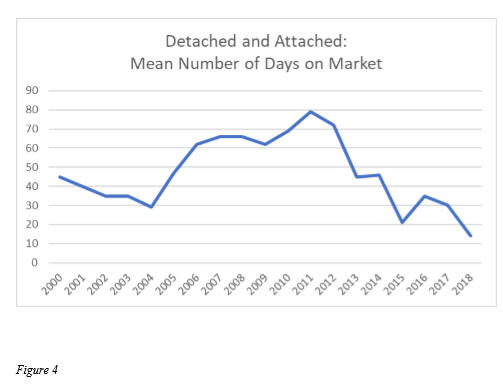

Market Overview: The mean number of days a property is on the market, based on first quarter data, will establish a new low of 14 days in 2018. In 2011, that number peaked at 79 days on market. In 2015, the number of days on market hit a then all-time low of 21 (see Figure 4).

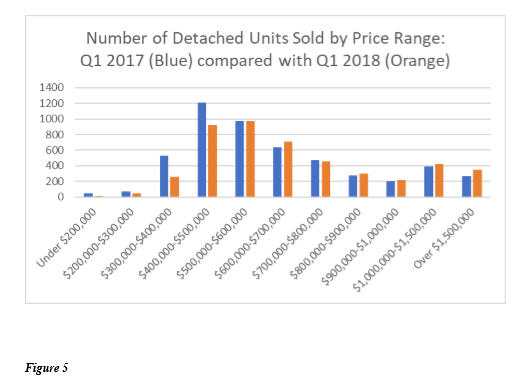

Detached Housing Market Specifics – 1st Quarter 2018 compared with 1st Quarter 2017: Detached home sales data for the 1st quarter of 2018 shows the highest number of sales were in the $500,000-$600,000 price range (969 units). This is an upward shift from last year when highest number of sales for the 1st quarter of 2017 were in the $400,000-$500,000 price range (1,211 units – see Figure 5).

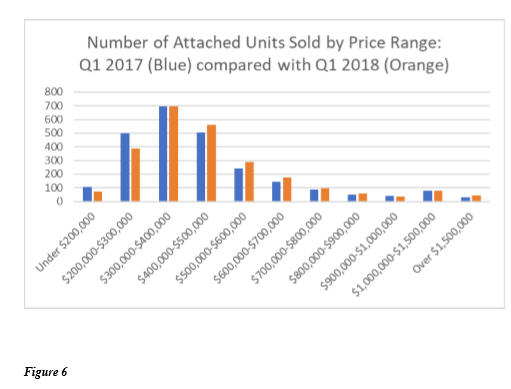

Attached Housing Market Specifics – 1st Quarter 2018 compared with 1st Quarter 2017: Attached home sales data for the 1st quarter of 2018 shows the highest number of sales were in the $300,000-$400,000 price range (696 units). The highest number of sales for the 1st quarter of 2017 were in the same $300,000- $400,000 price range (697 units) (see Figure 6).

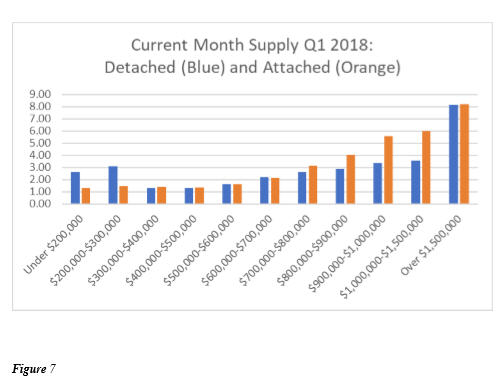

Detached and Attached Housing Market Specifics – 1st Quarter 2018 Housing Supply: Normal residential real estate markets typically have a six to seven-month supply of housing inventory. Based on 1st quarter 2018 absorption rates, current supply levels for detached properties are at (or below) normal market levels across all price except the $1,500,000 and up category. Similarly, current supply levels for attached properties are at (or below) normal market levels across all price ranges except the $1,500,000 and up category (see Figure 7).

Detached and Attached Housing Market Specifics – 1st Quarter 2018 Housing Supply: Normal residential real estate markets typically have a six to seven-month supply of housing inventory. Based on 1st quarter 2018 absorption rates, current supply levels for detached properties are at (or below) normal market levels across all price except the $1,500,000 and up category. Similarly, current supply levels for attached properties are at (or below) normal market levels across all price ranges except the $1,500,000 and up category (see Figure 7).

Comments and Outlook: Based on the first quarter MLS data, in 2018 the San Diego County housing market’s sales prices are on pace to increase by 3.3 percent over those of 2017. The county’s mean sales price is set to reach a new high of $689,017, surpassing the previous high set in 2017 (see Figure 3). Sales volume, absorption rates and days on market are on pace to decrease, year over year (see Figures 1, 2 and 4).

Inventory levels increased in the first quarter of 2018 over the last quarter of 2017 by 35%. However, supply levels of active listings across all price ranges are still at relatively low levels (see Figure 7).

The highest concentration of detached housing sales includes inventory priced below $600,000 (see Figure 5). The highest concentration of attached housing sales includes inventory priced below $500,000 (see Figure 6). Most sales activity continues to remain in these relatively lower price ranges, which is largely comprised of entry level housing.

Housing supply is below normal levels in most price ranges which will likely cause a continuation of a competitive environment for buyers during the second quarter of 2018, assuming interest rates remain relatively stable. Many real estate professionals continue to report multiple offers on entry level listings with a continuation of a two-tiered market: Multiple offers are being reported on fixer properties which have the potential for renovation and resale. Multiple offers are also being reported on renovated houses that are priced competitively. Based on the first quarter data, the expectation in 2018 is for an increase in sales prices with a reduction in the number of homes sold. Subsequent reports will continue to analyze the trends in local housing supplies, sales volume and sales prices.

Comments are closed.